Advertising in the Insurance sector in India – understanding the legal implications

After two decades, the IRDAI has proposed a modification to its regulations on advertising insurance products in India. What are the existing regulations? What are the modifications proposed by IRDAI? What are the do’s and don’ts that govern advertising in the Insurance sector? Part 24 of the series of articles on Misleading Ads by Advocate Aazmeen Kasad, is the first part of a series on Advertising in the Insurance sector in India, and serves to demystify and provide an in-depth understanding of what the law on the same is.

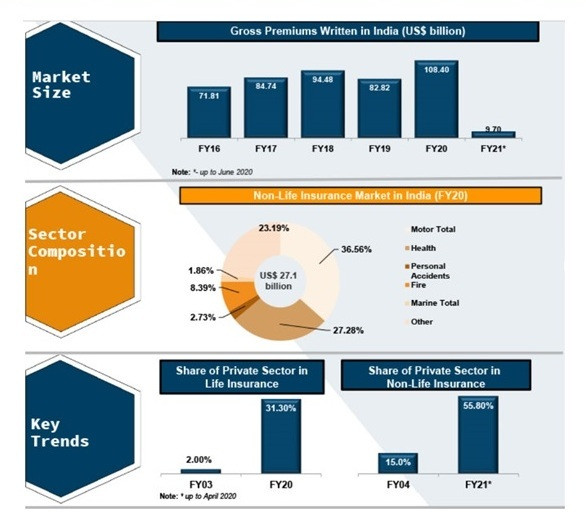

Insurance is broadly divided into life and non-life products. Advertising in the Insurance industry has witnessed a sea-change from the time that Insurance was exclusively controlled by the public sector, to today, when privatisation has ensured that a raft of players (24 life insurance and 33 non-life insurance companies in the Indian market), are vying for a slice of the Indian insurance pie; competing on price and services to attract customers. Per IBEF, the insurance industry in India was expected to reach $280 billion by the end of 2020. The life insurance industry in the country is expected to grow 12-15% annually over the next three to five years.

Source: IBEF Report

The success of insurance sales communication depends on public confidence and the faith they repose in the insurers, when they receive a communication from Insurers promoting their products. As such, the Insurers are expected to adopt fair, honest and transparent practices in the market-place and avoid practices that tend to impair the confidence of the public. As it may be difficult for the public to understand and evaluate the inherent details in the various insurance products, it is of paramount importance that the publicity material is relevant, fair and in simple language enabling informed decision making about whether or not to buy a specific insurance product. The verbal communication that the prospects receive from the agents/ intermediaries can be supplemented by the written material that is made available to them and also serve as authentic reference material. (Source: IRDAI)

Being a regulated industry in India, advertising Insurance products are governed by the Insurance Regulatory and Development Authority of India (IRDAI), who has notified that Insurance Regulatory and Development Authority (Insurance Advertisements and Disclosure) Regulations, 2000 (‘Regulation’), the Master Circular on Insurance Advertisements, the Consumer Protection Act, 2019 and the Advertising Standard Council of India’s Code on Self-Regulation in Advertising, to protect the interests of the public, enhance their level of confidence on the nature of sales material used and ultimately encourage fair business practices.

Advertisements in the Insurance sector are classified as either (i) Institutional advertisements; or as (ii) Insurance advertisements.

An ‘Institutional Advertisement’ does not, either directly or indirectly, intend to solicit the insurance business, but only promotes the brand image of the insurers and/or its intermediaries and may contain the registered name, address, toll-free number, logo or trademark thereof. Advertisements issued in any mode, including those that highlight sponsorships, fall under this category.

Any inclusion of product names or information about the products, performance of the companies or their funds, or the information about the product launches constitutes ‘insurance advertisements’.

What differentiates an insurance advertisement from other ads? As per the Regulation, an ‘insurance advertisement’ means and includes any communication directly or indirectly related to a policy and intended to result in the eventual sale or solicitation of a policy from the members of the public, and shall include all forms of printed and published materials or any material using the print and or electronic medium for public communication such as:

- i) newspapers, magazines and sales talks;

- ii) billboards, hoardings, panels;

iii) radio, television, website, e-mail, portals;

- iv) representations by intermediaries;

- v) leaflets;

- vi) descriptive literature/ circulars;

vii) sales aids flyers;

viii) illustrations form letters;

- ix) telephone solicitations;

- x) business cards;

- xi) videos;

xii) faxes; or

xiii) any other communication with a prospect or a policyholder that urges him to purchase, renew, increase, retain, or modify a policy of insurance.

From a reading of the above, it is clear that the definition of the term ‘Insurance Advertisement’ is illustrative and not exhaustive in nature. It is wide enough to include communication which could be direct or indirectly related to a policy and for public communication, across different forms of traditional and digital media.

An explanation to the provision serves to clarify on what does NOT constitute an insurance advertisement. Accordingly, (i) materials used by an insurance company within its own organisation and not meant for distribution to the public; (ii) communications with policyholders other than materials urging them to purchase, increase, modify surrender or retain a policy; (iii) materials used solely for the training, recruitment, and education of an insurer's personnel, intermediaries, counsellors, and solicitors, provided they are not used to induce the public to purchase, increase, modify, or retain a policy of insurance, (iv) any general announcement sent by a group policyholder to members of the eligible group that a policy has been written or arranged; so long as they are not used to induce the purchase, increase, modification, or retention of a policy of insurance.

In contrast, under, section 2(1) of the Consumer Protection Act, 2019, an ‘advertisement’ means any audio or visual publicity, representation, endorsement or pronouncement made by means of light, sound, smoke, gas, print, electronic media, internet or website and includes any notice, circular, label, wrapper, invoice or such other documents. Therefore, this includes advertisements not only on the traditional media such as print, radio or television advertisements, but also includes packaging, point of sale material, etc. Advertisements on the Internet, including social media such as ads posted on Facebook, Instagram, Twitter, LinkedIn, etc., also fall within the purview of the Act, as do advertisements on websites, which includes the advertiser’s own website(s).

Per the Regulations, an “unfair or misleading advertisement” will mean and include any advertisement:

(i) that fails to clearly identify the product as insurance;

(ii) makes claims beyond the ability of the policy to deliver or beyond the reasonable expectation of performance;

(iii) describes benefits that do not match the policy provisions;

(iv) uses words or phrases in a way which hides or minimises the costs of the hazard insured against or the risks inherent in the policy;

(v) omits to disclose or discloses insufficiently, important exclusions, limitations and conditions of the contract;

(vi) gives information in a misleading way;

(vii) illustrates future benefits on assumptions which are not realistic nor realisable in the light of the insurer’s current performance;

(viii) where the benefits are not guaranteed, does not explicitly say so as prominently as the benefits are stated or says so in a manner or form that it could remain unnoticed;

(ix) implies a group or other relationship like sponsorship, affiliation or approval, that does not exist; or

(x) makes unfair or incomplete comparisons with products which are not comparable or disparages competitors.

Under the Consumer Protection Act, 2019, a ‘misleading advertisement’ in relation to any product or service, is an advertisement, which (i) falsely describes such product or service; or (ii) gives a false guarantee to, or is likely to mislead the consumers as to the nature, substance, quantity or quality of such product or service; or (iii) conveys an express or implied representation which, if made by the manufacturer or seller or service provider thereof, would constitute an unfair trade practice; or (iv) deliberately conceals important information. Thus, any advertisement which expressly or impliedly misleads consumers about the product or service will also be considered as misleading in nature.

Under the Consumer Protection Act, the Central Consumer Protection Authority will regulate matters relating to violation of rights of consumers, unfair trade practices and false or misleading advertisements which are prejudicial to the interests of public and consumers to promote, protect and enforce the rights of consumers. This Authority is headquartered in the National Capital Region of Delhi and may have regional and other offices across India.

A complaint relating to any false or misleading advertisements may be forwarded either in writing or in electronic mode, to any one of the authorities, namely, the District Collector or the Commissioner of regional office or the Central Authority. After a preliminary enquiry is made, if the Central Authority is satisfied that a prima facie case exists, an investigation shall be conducted.

Where the Central Authority is satisfied after conducting the investigation that the advertisement for which a complaint is received is false or misleading and is prejudicial to the interest of any consumer or is in contravention of consumer rights, it may, by order, issue directions to the concerned trader or manufacturer or endorser or advertiser or publisher, as the case may be, to discontinue such advertisement or to modify the same in such manner and within such time as may be specified in that order. If the Central Authority is of the opinion that it is necessary to impose a penalty in respect of such false or misleading advertisement, by a manufacturer or an endorser, it may, by order, impose on manufacturer or celebrity endorser a penalty which may extend to Rs 10 lakh: Provided that the Central Authority may, for every subsequent contravention by a manufacturer or endorser, impose a penalty, which may extend to Rs 50 lakh. Additionally, where the Central Authority deems it necessary, it may, by order, prohibit the celebrity endorser of a false or misleading advertisement from making endorsement of any product or service for a period which may extend to one year: For every subsequent contravention, prohibit such endorser from making endorsement in respect of any product or service for a period which may extend to three years. Where the Central Authority is satisfied after conducting an investigation, that any person is found to publish, or is a party to the publication of a misleading advertisement, except in the ordinary course of his business, it may impose on such person a penalty which may extend to Rs 10 lakh. The defence that the false or misleading advertisement was published in the ordinary course of business shall not be available to such person if he had previous knowledge of the order passed by the Central Authority for withdrawal or modification of such advertisement.

In light of the newly introduced provisions under the Act, which came into force from July 20, 2020, it is advisable for both the advertisers and the endorsers to exercise caution in the claims that form part of the advertisement of the goods/ services. The ensuing Parts of the series will pertain to various aspects of what constitutes Misleading Advertising and key judicial precedents on the same.

Advocate Aazmeen Kasad is a practicing corporate advocate with over 20 years of experience, with a focus on the Media, Technology and Telecom industries. She is also a professor of law since 14 years. She is a member of the Consumer Complaints Council of the Advertising Standards Council of India. She is a speaker at several forums.

Share

Facebook

YouTube

Tweet

Twitter

LinkedIn